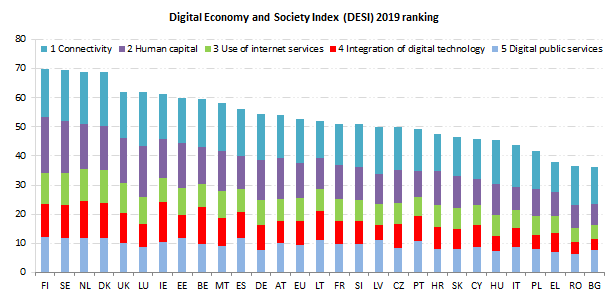

The European Commission this month released the results of the 2019 Digital Economy and Society Index (DESI) Report, which monitors Europe’s overall digital performance and tracks the progress of EU countries with respect to their digital competitiveness.

Countries that have set up ambitious targets in line with the EU Digital Single Market Strategy and combined them with adapted investment achieved a better performance in a relatively short period of time. This is one of the main conclusions of this year’s Digital Economy and Society Index (DESI). However, the fact that the largest EU economies are not digital frontrunners indicates that the speed of digital transformation must accelerate, in order for the EU to stay competitive at world level.

Vice-President for the Digital Single Market Andrus Ansip, said: “In late 2014, when we began drawing up a plan for the Digital Single Market we wanted to build a long-term strategy to stimulate Europe’s digital environment, minimise legal uncertainty and create fair conditions for everyone. Now that the EU has agreed on 28 out of 30 legislative proposals, creating 35 new digital rights and freedoms, the successful implementation of the Digital Single Market can significantly contribute to further improving country results. It is urgent to implement new rules to boost connectivity, data economy and digital public services as well as help Member States to equip citizens with digital skills that are adapted to the modern labour market”.

Commissioner for the Digital Economy and Society, Mariya Gabriel, added: “This year’s Digital Economy and Society Index demonstrates that the speed of digital transformation must accelerate for the EU to stay competitive at world level. In order to succeed, we have to continue to work together for an inclusive digital economy and ensure unimpeded access to digital skills for all EU citizens in order to truly thrive and build a more digital Europe.”

DESI figures over the last 5 years show that targeted investment and robust digital policies can have a significant impact on the performance of individual countries. For example, this is the case for Spain, in the deployment of ultrafast broadband, Cyprus in broadband connectivity, Ireland for digitizing businesses and Latvia and Lithuania in digital public services.

Connectivity has improved, but remains insufficient to address fast-growing needs. DESI indicators show that the demand for fast and ultrafast broadband is on the rise, and is expected to further increase in the years in view of the growing sophistication of internet services and business needs. Ultrafast connectivity of at least 100 Mbps is available to 60% of households, and the number of broadband subscriptions is increasing. 20% of homes use ultrafast broadband, a number that is four times higher than in 2014.

The EU has agreed on the reform of the EU telecoms rules to meet Europeans’ growing connectivity needs and to boost investments. Sweden and Portugal have the highest take-up of ultrafast broadband, and Finland and Italy are the most advanced on the assignment of the 5G spectrum.

More than one third of Europeans in the active labour force do not have basic digital skills, even though most jobs require at least basic digital skills, and only 31% possess advanced internet user skills. At the same time, there is an increased demand for advanced digital skills across the economy, with employment of Information and Communication Technology (ICT) specialists growing by 2 million over the last 5 years in the EU.

Finland, Sweden, Luxembourg and Estonia are the leaders in this dimension of the index.

83% of Europeans surf the internet at least once per week (up from 75% in 2014). On the other hand, a mere 11% of the EU population have never been online (down from 18% in 2014).

The use of video calls and video on demand, available on various computer programmes and smartphone applications, increased most. To better protect users’ trust in the online environment, EU rules on data protection entered into force on 25 May 2018.

Businesses are becoming more digital, but e-commerce is growing slowly. Overall, the top EU performers in this domain are Ireland, the Netherlands, Belgium and Denmark, while Hungary, Romania, Bulgaria and Poland need to catch up.

An increasing number of companies use cloud services (18% compared to 11% in 2014) and social media to engage with their customers and other stakeholders (21% compared to 15% in 2013). However, the number of SMEs who sell their goods and services online has stagnated over the past few years at 17%.

In order to boost e-commerce in the EU, the EU has agreed on a series of measures from more transparent parcel delivery prices to simpler VAT and digital contract rules. Since 3 December 2018, consumers and companies are able to find the best online deals throughout the EU without experiencing discrimination based on their nationality or place of residence.

In the digital public services, where EU regulation is in place, there is a convergence trend among Member States for the period 2014-2019.

Sixty-four per cent of internet users who submit forms to their public administration now use online channels (up from 57% in 2014), showing the convenience of online procedures over bureaucracy.

In April 2018, the Commission adopted initiatives on the re-use of public sector information and on e-health, which will significantly improve cross-border online public services in the EU.

With regards to the use of digital public services, including e-health and e-government, Finland and Estonia registered the highest scores in the index.

Also released in June, the Women in Digital Scoreboard, shows that EU countries who are digitally competitive are also leaders in female participation in the Digital Economy.

Finland, Sweden, Luxembourg and Denmark have the highest scorers regarding the participation of women in the digital economy. The gender gap, however, persists at EU level in the areas of internet use, digital skills, and ICT specialist skills and employment with the largest inequalities in the latter: only 17% of ICT specialists are women, and they still earn 19% less than what men earn. In addition, only 34% of ´STEM (science, technology, engineering and mathematics) graduates are women, a figure we need to increase in the years to come.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}